By Brian H. Graff

This article originally appeared in the Spring 2013 issue of 403(b) Advisor Magazine. To view a PDF copy of this article, please click HERE.

Policymakers won’t be able to improve America’s retirement system if they base their decisions on these five misconceptions.

Our goal as retirement professionals should be to increase the number of workers saving for retirement and the amount these workers are saving. The question is: How do we get there in the most efficient and effective way? An enhanced Saver’s Credit would help lower-income workers who are already participating save more, but by itself it won’t substantially benefit those workers who aren’t covered by a plan and not saving in the first place.

What we know works is automatic enrollment in a workplace retirement plan. Moderate-income workers are 15 times more likely to save when covered by a 401(k) plan than when their only option is to save on their own in an IRA. So the policy objective should be how to increase the availability of retirement savings plans at work.

The current tax incentives encourage employers to adopt a retirement plan such as a 401(k) plan and encourage employees to save in these plans. Congress saw fit to provide certainty about the availability of these tax incentives when it overwhelmingly passed the Pension Protection Act in 2006 with bipartisan support. These incentives have been extremely effective at providing retirement savings to tens of millions of American workers.

The first step in securing future retirement security is to do no harm to what has been working very well. Some proposals that have been raised in the context of deficit reduction or tax reform would seriously hurt coverage and reduce the level of retirement savings across income groups. Small businesses would be hurt the worst. Proposals currently under discussion— whether slashing the contribution limits, reducing tax incentives or turning the current year’s exclusion into a credit — would discourage small-business owners from setting up or maintaining a workplace retirement plan. That’s the exact opposite of what needs to be done.

There are some persistent, I would say dangerous, myths that fuel these misguided proposals.

Myth #1: Incentives for Retirement Savings are Tax Expenditures

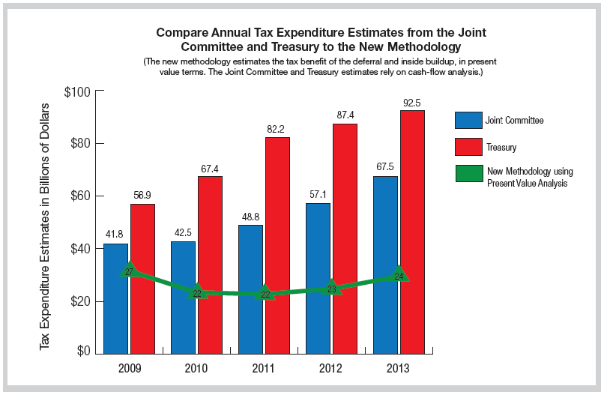

Incentives for retirement savings don’t belong in the same category as most other deductions or exclusions classified as “tax expenditures.” Unlike deductions for mortgage interest or charitable contributions, which are permanent deductions, the incentives for retirement savings are just a deferral. Contributions (and earnings) are taxed at ordinary income rates when they’re distributed from the plan.

By ignoring the present value of future taxes paid on those distributions, the revenue that appears to be gained in the budget window from cutting retirement savings incentives is an illusion. In fact, a study by two former Joint Committee on Taxation staffers showed the true present-value cost of 401(k) incentives to be close to a third of the cost reported by Treasury. Reduced contributions today mean lower revenue outside the budget window, when there will be less retirement savings to be withdrawn and taxed. In other words, bad math leads to bad retirement policy.

Myth #2: Current Tax Incentives Haven’t Worked to Encourage Workplace Savings

Coverage statistics based on all workers are used to allege that current tax incentives have failed, but the relevant facts show otherwise. The current incentives under the Code and ERISA are targeted at full-time workers, and have been very successful at extending coverage to the full-time workforce. Bureau of Labor Statistics data shows 78% of all full-time workers have access to a workplace retirement plan, with 84% of those workers participating.

Current law provides for the exclusion of part-time workers and it’s simply unfair to judge the 401(k) system for what current law provides; 80% coverage of full-time workers is a success story.

Myth #3: The Current Tax Incentive is ‘Upside Down’

This myth arises from a failure to understand how the incentives for workplace retirement plans really work. Nondiscrimination rules require plans to satisfy proportionality tests to make sure that retirement plan benefits don’t discriminate in favor of the highly paid. Further, current law already has a $250,000 cap on the amount of compensation that can be considered in determining benefits.

I’m not suggesting that the mortgage deduction should be available only to highly compensated taxpayers if they can prove non-highly compensated people in their office also benefit. But that’s what would happen if you applied the same retirement plan nondiscrimination standards to those other tax incentives.

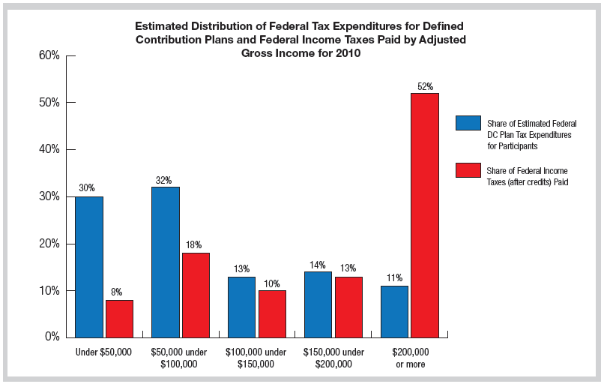

The result of these nondiscrimination rules is that the current tax incentive for defined contribution plans is more progressive than the current income tax system itself. Based on an analysis by a former JCT economist, taxpayers making less than $50,000 pay only 8% of income taxes, but receive 30% of the tax incentives for defined contribution plans. Households making less than $100,000 pay 26% of income taxes, but get more than 60% of the benefit of this tax incentive. By contrast, households making more than $200,000 pay 52 percent of all income taxes, but receive only 11% of retirement plan tax incentives.

More than 60 percent of a tax incentive going to workers who pay less than 30% of income taxes is not upside down. It is very much right side up.

Myth #4: Small Businesses Will Sponsor Retirement Plans Without an Appropriate Tax Incentive

The current year’s tax savings is a critical factor — often the only factor — supporting a small-business owner’s decision to put in a plan. That’s not to say that small-business owners are selfish, or don’t want to help their employees save for retirement. However, most small-business owners are short on cash. To put in a plan, they need to figure out how to pay for it. Especially these days, they use the savings generated from the retirement plan tax incentives to help pay for contributions (such as a match) required by the nondiscrimination rules. Reducing the incentive literally reduces the cash the small-business owner has to work with. Reduced incentives will mean fewer plans and lower employer contributions for those remaining plans.

Myth #5: It Doesn’t Matter if a New Tax Structure Causes Employers to Terminate Plans Because ‘Re-engineering the Tax Incentive Will Lead More Workers to Save on their Own’

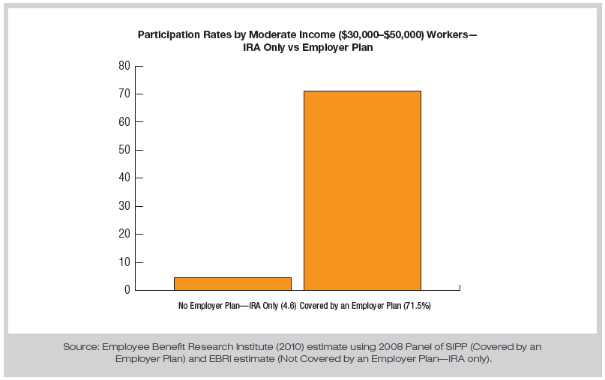

The truth is, the only way we’ve ever gotten working Americans to save for retirement is through employer-sponsored retirement plans. More than 70% of workers making $30,000 to $50,000 contribute when covered by a plan at work. By comparison, less than 5% of workers at the same income levels save on their own in an IRA when there is no workplace plan.

Changing the exclusion to a credit will never make up this dramatic difference in savings rates. Increasing plan coverage is a much simpler task with more certain results.

The key to promoting retirement security is expanded workplace savings. Reduced incentives for small-business owners to sponsor retirement plans would be a big step in the wrong direction, and would not produce the long-term savings needed to balance the nation’s budget. We need to focus on proposals like the auto-IRA bill offered by Rep. Richard E. Neal (D-Mass.) to bring workers into the workplace saving system. The deferral nature of the current tax incentives means today’s tax break is tomorrow’s tax revenue. Let’s build the system up, not tear it down.

***

Brian H. Graff , Esq., APM, is executive director and CEO of the American Society of Pension Professionals & Actuaries in Arlington, Va.

Recent Comments

Does the roth requirement for catch-up contributions for people who earned $145,000 apply to 457...

Hi Ed,

I really liked this article and I think you make a lot of sense. And I had no...

I believe there's a misstatement in that last quote - it should refer to governmental and...

Working with several medical providers as clients, I note that the high-end earners tend to push...

Congratulations to NTSAA for landing a good one. Nathan's breadth of experience and...